3 Best College Funds to Maximize Saving for College

When you’re ready to begin saving for your little one’s future education, you’ll find a number of options. Choosing the right one for your specific needs can feel overwhelming since each education savings vehicle comes with its own set of benefits and drawbacks.

Fortunately, saving for college for your baby doesn’t have to be stressful. You simply need to know what the best college savings programs are and how to start saving with them.

1. 529 Plan

529 plans, such as the NC 529 Plan, are tax-advantaged because they allow you to save after-tax dollars that can then grow tax-free. As long as you use the money from your child’s account for qualified educational expenses, you’ll never have to pay any state or federal taxes on the earnings. In addition to the tax benefits, let’s discuss even more benefits of 529 plans.

529 Benefits

- No age restrictions or income limitations. No matter how much money you make, you can open an NC 529 Account for your child, grandchild, or even yourself. Better still, if the account holder doesn’t need the funds, the money can be used for another family member’s education expenses — without penalty.

- High contribution limits. Because each state sets its own total contribution limit for 529 plans, there isn’t one fixed amount, but most range between $235,000 and $529,000. These amounts are determined based on Maximum Projected Expenses for college. For instance, NC 529 bases the Maximum Projected Expenses on what it would cost to attend four years of undergraduate and three years of graduate or professional study at the most expensive schools in North Carolina (though the funds from an NC 529 Account can be used at any eligible in- or out-of-state institution). Currently, NC 529 allows a maximum of $550,000 per beneficiary, one of the highest account limits of any 529 plan in the country.

- Anyone can contribute to a 529 plan. That means relatives, friends, and even your employer can all chip in to fund your child’s educational endeavors. NC 529 has made gifting especially easy. Once a user activates their personalized gifting link, they can share it with friends and family members, who can then contribute to the account at any time.

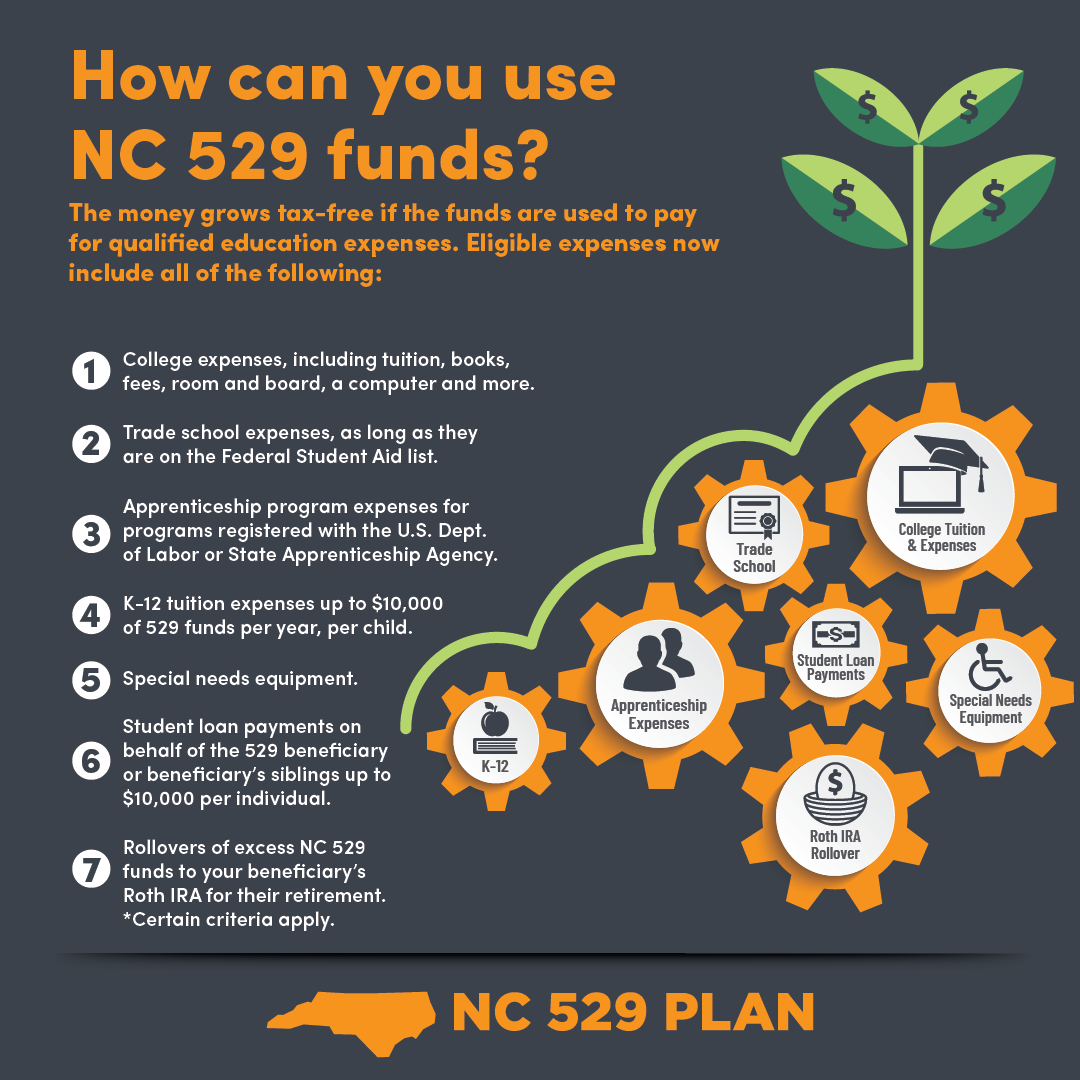

- Funds can be used on a long list of qualified expenses. In addition to many college expenses (such as tuition, room and board, books, and the cost of a computer), 529 funds can also be used for trade school or apprenticeship program expenses, tuition for private K–12 schools, special needs equipment, student loan payments, and more.

- Unused funds can be rolled over tax-free into a Roth IRA. That’s right. Excess money from your NC 529 Account can now be used to save for your beneficiary’s retirement as long as the funds meet certain criteria. So, one of the best college savings programs can now be used to fund your beneficiary’s retirement as well!

- 529 plans don’t have a negative impact on financial aid. Although an NC 529 Account held for the benefit of a dependent student does have to be reported on the Free Application for Federal Student Aid (FAFSA), it’s counted as a parental asset. As such, it’s assessed at a much lower rate (up to 5.64%) than the student’s assets (up to 20%) in determining financial aid.

{kind=link}

Drawbacks

- Funds can only be used for qualified education expenses. If you withdraw the money for a non-qualified expense (such as buying a car for the beneficiary), you’ll be required to pay federal and state taxes on the earnings portion of the withdrawal plus a 10% penalty.

- Your investment options may be limited with some 529 plans. Because every 529 plan is different, some states may have options that are too conservative for your taste, while others may have more risk than you’re comfortable with. NC 529 offers conservative, moderate, and aggressive tracks, so you can choose the one that best suits your child’s needs and your comfort level. Check with your financial advisor to find the best plan for your budget.

2. Coverdell Education Savings Account (ESA)

Formerly called the Education IRA, the Coverdell ESA is somewhat similar to a 529 plan. It’s also tax-advantaged in that it offers tax-free growth on your investments and withdrawals for qualified education expenses. However, not everyone is eligible to open an account, and the contribution levels are more limited.

Benefits

- Anyone can contribute to your child’s Coverdell ESA, but the contributor must meet certain modified adjusted gross income requirements established by the IRS.

- Funds can be used for a variety of qualified education expenses. These include tuition and fees, books, supplies, and other equipment at K–12 schools, colleges, universities, or vocational programs.

- There are a wide variety of investment options, including some that are self-directed.

Drawbacks

- Not everyone is eligible to contribute to a Coverdell ESA. If you’re an individual earning more than $110,000 or part of a married couple earning more than $220,000 annually, you can’t contribute to a Coverdell ESA for your child.

- Contribution levels are low. The total maximum contribution is $2,000 per year per beneficiary.

- There are age restrictions. All contributions must be made before the beneficiary turns 18. Additionally, all assets must be used for qualified education expenses before the beneficiary turns 30, or the funds may be forced out and incur a 10% penalty.

- Coverdell ESAs may negatively impact financial aid. There are some cases where the funds may be treated as the student’s assets (up to 20%) on the FAFSA.

3. Qualified U.S. Savings Bonds

One of the most conservative ways to save for college is to invest in U.S. savings bonds. Series EE and Series I are the two that offer tax benefits for higher education expenses.

Benefits

- Savings bonds are a safe investment. Backed by the U.S. government, EE bonds are guaranteed to double within 20 years, and I bonds earn a fixed rate that adjusts with inflation.

- Bonds are tax-exempt when you use them to pay for qualified education expenses unless you make more than the IRS cut-off allows (see below).

- Bonds offer flexibility. When you purchase bonds with different maturity dates, you’ll know approximately how much money you’ll have available when your child needs it for college.

Drawbacks

- Bonds offer a lower rate of return than most other investments. While some people may like the low-risk aspect of bonds, that benefit generally comes with the disadvantage of a low reward.

- Maximum yearly investment is limited. An individual can invest $10,000 per year per type of bond ($20,000 for a couple).

- Earnings not spent on qualified education expenses are subject to federal and state taxes.

- Not everyone qualifies for the tax break. If your modified adjusted gross income (MAGI) is more than the cut-off set by the IRS, your earnings will be taxed, even if you spend them on qualified education expenses.

- The owner of the bond must be 24 or older when the bond is issued. That means a parent must be the owner of the bond, not the child.

Start Saving Now

No matter how you do it, the important thing is to start saving for college as soon as possible. NC 529 is one of the best tax advantaged college savings plans available. There are no enrollment fees, and we make it easy for you to get started. With just $25 and a few minutes, you can open an NC 529 Account and begin saving for your child’s future education today.