College Fund for Grandchildren: How to Set Up a 529

Set Up a College Fund for Your Grandchildren

The cost of a college education is on the rise, and many grandparents are asking themselves what they can do to help their grandchildren plan for the future. If this is you, you’re not alone. According to a report in The Charlotte News, more than half of grandparents are helping pay or plan to help pay for their grandchildren’s college.

Planning for your grandchild’s education is a tremendous gift. It can set your grandchild on the path to success and reduce debt for them and their parents. If you’re planning to open the account yourself and be the primary contributor, let’s look at some options so your money can have the maximum benefit for your grandchild’s future.

Options for a College Fund for Grandchildren

There are several savings options you can choose from to save for a grandchild’s education.

- Savings Account – There’s nothing wrong with a good old-fashioned savings account at your local bank. You can keep the account in your name and name the grandchild as the beneficiary. However, these types of accounts generally offer low interest rates.

- Custodial Account – This type of account names the child as the owner and the grandparent as the custodian. You will manage the account until the child becomes an adult. In North Carolina, a teen reaches adulthood at age 18. At that point, your grandchild controls the money and can do anything they want with it, which may not include your wishes that they go to college. The most common type of custodial account is a Coverdell Education Savings Account (ESA).

- NC 529 Account – Nearly every state has a 529 plan option for families to save for K–12 tuition and college expenses. In North Carolina, we have the NC 529 Plan. It’s a tax-advantaged education savings account that allows earnings to grow tax-free when the money is used for qualified education expenses. The person who opens the account is the owner or participant, and the child is generally named as the beneficiary. The child does not gain access to the money when they become an adult unless you transfer ownership of the account to them.

How Can I Open a 529 For My Grandchildren?

If you have more than one grandchild, it’s recommended that you open a separate NC 529 Account for each child. You can be the account owner of multiple accounts and retain control over financial decisions related to each account.

Opening a college fund for grandchildren with NC 529 is a simple process. You will need some basic information about the beneficiary, including their Social Security Number (SSN) or Taxpayer Identification Number (TIN), birth date, address, email address, and a minimum $25 contribution. After that, how you fund the account is up to you.

Making Contributions:

You can write a personal check to make one-time contributions for college gifting, or you can set up automatic withdrawals from your bank account. If you own the account, you can also send the unique gifting link to other friends and family so they can contribute as well.

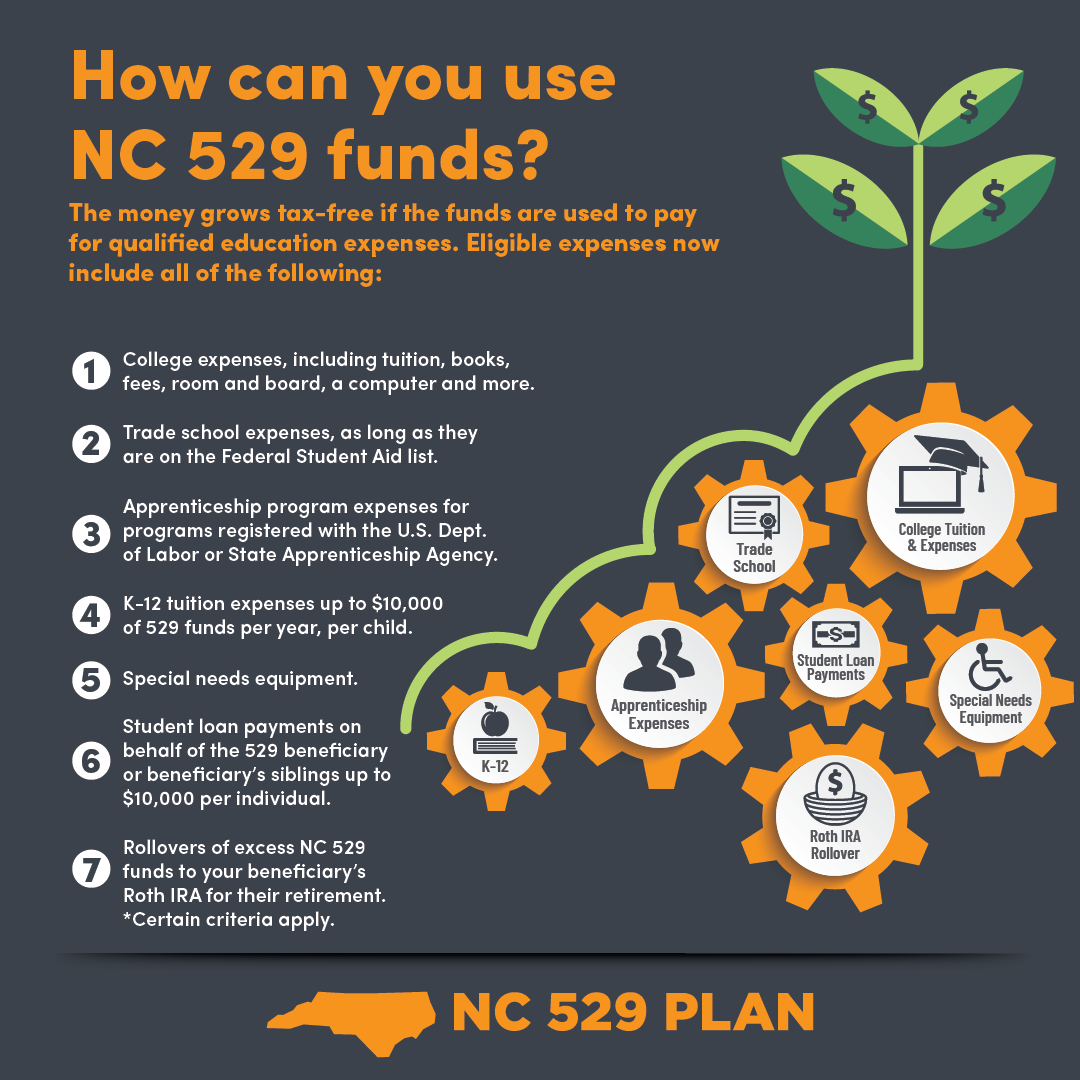

Using Funds for Qualified Education Expenses:

For the funds to grow tax-free, they need to be used for qualified education expenses. These are essential education needs, including:

{kind=link}

- K–12 tuition

- College tuition, room and board, and supplies

- Career and technical programs

- Special needs equipment

- Student loan payments, and more.

Contribution Limits:

Be mindful of gifting tax limits. You can contribute up to $18,000 a year ($36,000 for married couples) to each grandchild’s account. You can also superfund the account, which simply means depositing five years of contributions all at once. For an individual, that would equal $90,000 ($180,000 for married couples). Discuss your saving strategy with a financial advisor.

There are also overall account limits. Currently, the maximum amount for an NC 529 Account is $550,000.

What if My Grandchild Doesn’t Go to a Four-Year College?

The path your grandchild chooses may not mean attending a four-year college or university. And that’s okay because NC 529 is flexible!

Your grandchild can still get the tax benefits if they use the funds to pay for community college programs, trade school, and eligible apprenticeship programs. The funds also don’t expire. If your grandchild decides they don’t want to go to college right after high school, the funds will be waiting if they change their mind.

What Happens if There are Leftover Funds?

If a grandchild decides not to use the account, or there are leftover funds, the money can be transferred to another family member to continue their education. Additional funds, with limitations, can also be rolled over into a Roth IRA for the beneficiary’s retirement.

Finally, if you want to withdraw the funds for non-educational expenses, that’s also an option. However, the earnings would be subject to a 10% penalty plus state and federal taxes.

Start Saving With NC 529

An education savings account is a wonderful gift to give to your grandchildren. It can help them graduate from college with as little debt as possible (or maybe none!) and give them a firm foundation to start building their life.

Ready to start a college fund for grandchildren? Open an NC 529 Account and start saving for the future.